Income Tax for Self-Employed in Spain: Calculation, Brackets and How to Pay Less (2026)

Self-employed income tax 2026: how it's calculated, brackets, form 130, tax deductions and strategies to legally pay less. Optimize now!

💡 Are you an employee? Calculate your income tax automatically

👉 Net salary calculator for employees

How does income tax work for self-employed?

Income tax for self-employed (autónomos) works differently than for employees. While salaried workers have automatic withholdings each month, self-employed must:

- Calculate their net income (revenue - expenses)

- Pay income tax quarterly through form 130

- File the annual tax return

- Settle accounts with the Tax Agency (refund or additional payment)

Key advantage: Self-employed can deduct expenses, which significantly reduces the income tax to pay.

Income tax brackets for self-employed (2026)

Income tax brackets are the same for self-employed as for employees, but they apply to net income (not gross billing):

| Net income | State rate | Regional rate (average) | Total approximate |

|---|---|---|---|

| Up to €12,450 | 9.50% | 9.50% | 19% |

| €12,450-€20,200 | 12.00% | 12.00% | 24% |

| €20,200-€35,200 | 15.00% | 15.00% | 30% |

| €35,200-€60,000 | 18.50% | 18.50% | 37% |

| €60,000-€300,000 | 22.50% | 22.50% | 45% |

| More than €300,000 | 24.50% | 22.50% | 47% |

Important: The regional rate varies by autonomous community. Madrid has lower rates, Catalonia higher.

Net income: the key to self-employed income tax

Unlike employees, self-employed pay income tax on net income, not on gross revenue.

Basic formula

Net income = Revenue - Deductible expenses

Practical example

If you bill €40,000 per year and have €10,000 in deductible expenses:

- Net income: €40,000 - €10,000 = €30,000

- Income tax to pay: ≈€6,500 (on €30,000, not on €40,000)

Savings: By deducting €10,000 in expenses, you save ≈€3,000 in income tax (30% of €10,000).

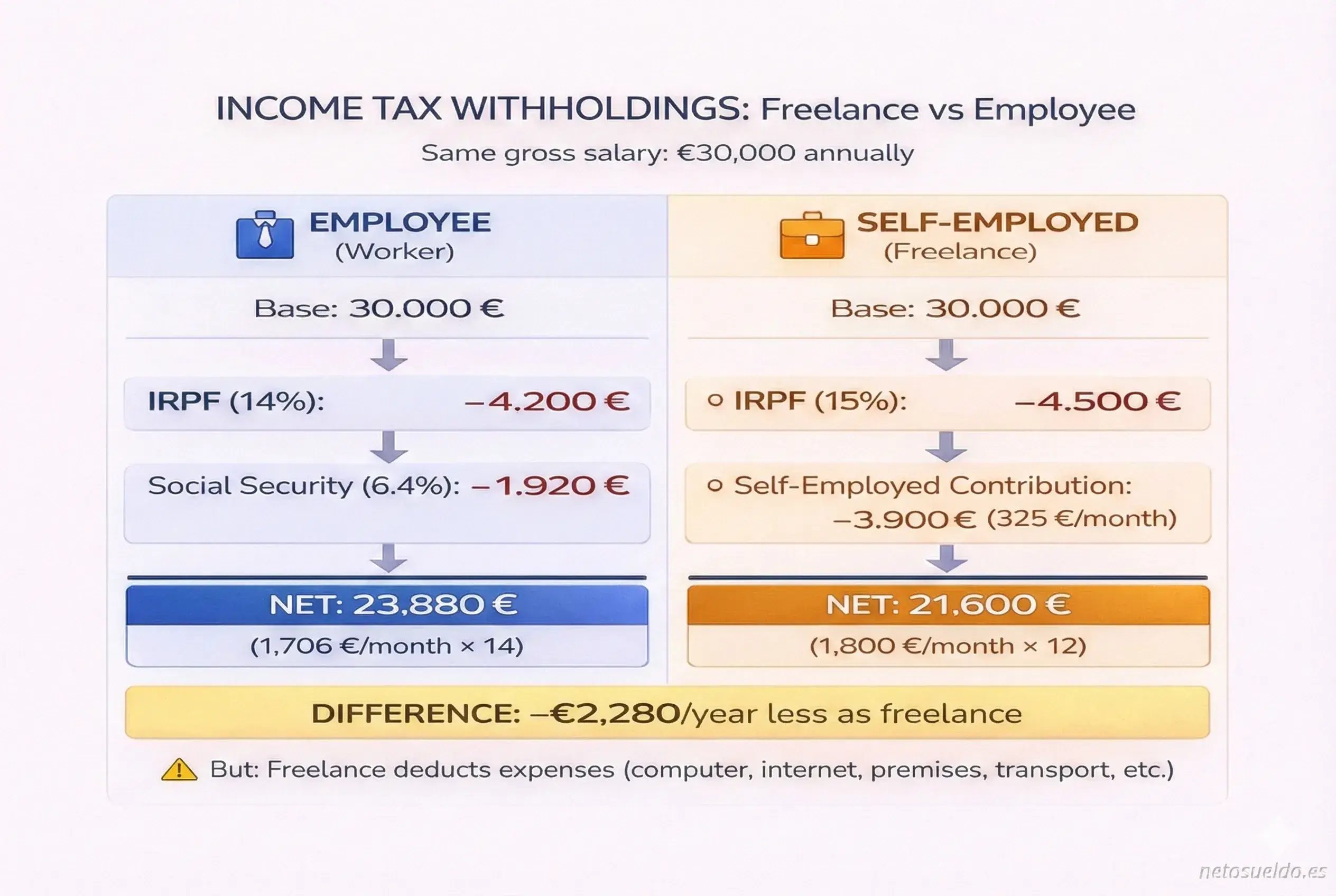

Self-employed vs Employee: Who pays more income tax?

As you can see, with the same gross salary, a self-employed person pays more in total (Social Security + income tax) than an employee. However, the key is to maximize deductions to reduce net income.

Deductible expenses that reduce your income tax

All these expenses subtract from your income and reduce income tax:

100% deductible expenses

✅ Self-employed Social Security contribution

✅ Accounting and tax advisory services

✅ Office supplies (computer, software, stationery)

✅ Office or coworking rent

✅ Internet and phone (if exclusive professional use)

✅ Advertising and marketing (website, Google Ads, brochures)

✅ Professional training (courses, masters, technical books)

✅ Work travel (transport, hotel, per diems)

✅ Professional insurance (liability, business multi-risk)

✅ Office utilities (electricity, water, if commercial premises)

✅ Financial expenses (interest on business loans)

✅ Equipment depreciation (computers, machinery)

Partially deductible expenses (working from home)

If you work from home, you can deduct 30% of:

✅ Utilities (electricity, water, gas)

✅ Internet and phone

✅ Homeowners association fees

✅ Property tax (IBI)

Example: If you pay €100/month for electricity, you can deduct €30/month = €360/year.

NON-deductible expenses

⚠️ Personal clothing (except specific professional uniforms)

⚠️ Daily meals (except on work trips)

⚠️ Traffic fines

⚠️ Personal expenses unrelated to the activity

⚠️ Corporate tax (if you're a self-employed individual)

Tip: Keep all invoices and receipts. Without proof, it's not deductible.

Form 130: quarterly installment payments

Form 130 is the quarterly income tax return for self-employed. It's filed 4 times a year:

Form 130 calendar (2026)

| Quarter | Period | Filing deadline |

|---|---|---|

| Q1 | January-March | April 1-22 |

| Q2 | April-June | July 1-22 |

| Q3 | July-September | October 1-22 |

| Q4 | October-December | January 1-30, 2027 |

How to calculate form 130

Income tax to pay = (Quarter revenue - Quarter expenses) × 20%

Important: You subtract previous quarter payments.

Practical example: Q1 calculation

Let's assume in the first quarter (January-March):

- Revenue: €12,000

- Deductible expenses: €3,000

Calculation:

- Net income: €12,000 - €3,000 = €9,000

- Quarterly income tax: €9,000 × 20% = €1,800 to pay

Practical example: Q2 calculation

In the second quarter (April-June):

- Cumulative revenue (Jan-Jun): €25,000

- Cumulative expenses (Jan-Jun): €6,500

- Paid in Q1: €1,800

Calculation:

- Cumulative net income: €25,000 - €6,500 = €18,500

- Cumulative income tax (20%): €18,500 × 20% = €3,700

- Already paid in Q1: -€1,800

- To pay in Q2: €1,900

Income tax withholding when invoicing

When you invoice Spanish companies, you can apply income tax withholding:

Common withholding rates

- General withholding: 15%

- New self-employed (first 3 years): 7%

- Agricultural/livestock withholding: 1-2%

- Professional withholding (architects, lawyers): 15-19%

What does invoicing with withholding mean?

If you invoice €1,000 + VAT with 15% withholding:

- Client pays: €1,000 + €210 (21% VAT) - €150 (15% withholding) = €1,060

- You receive: €1,060

- Client pays Tax Agency on your behalf: €150

Advantages of invoicing with withholding

✅ You don't file form 130 (quarterly) → better cash flow

✅ The client advances your income tax to Tax Agency

✅ Less administrative paperwork

✅ You settle accounts in the annual return

When you should NOT invoice with withholding

⚠️ Private clients (individuals)

⚠️ Clients outside Spain (EU or international)

⚠️ First 3 years as self-employed (you can apply 7% instead of 15%)

Annual tax return: final settlement

In April-June of the following year, you file the annual tax return (form 100). Here the Tax Agency:

- Calculates actual income tax based on your total annual net income

- Compares with what you've paid (form 130 or withholdings)

- Refunds you if you overpaid

- Charges you if you underpaid

Example: complete annual return

Year data:

- Total billing: €45,000

- Deductible expenses: €11,000

- Net income: €34,000

Quarterly income tax paid (form 130):

- Q1: €1,600

- Q2: €1,700

- Q3: €1,750

- Q4: €1,800

- Total paid: €6,850

Actual income tax (by brackets):

- First €12,450 at 19%: €2,365

- From €12,450 to €20,200 at 24%: €1,860

- From €20,200 to €34,000 at 30%: €4,140

- Total actual income tax: €8,365

Result:

- Actual income tax: €8,365

- Already paid: €6,850

- To pay in June: €1,515

Legal strategies to pay less income tax

1. Maximize deductible expenses

Before the year ends:

- Buy necessary equipment (computer, software)

- Pay training courses

- Prepay recurring expenses (accounting, insurance)

- Renew office supplies

Potential savings: 30-37% of the expense (according to your marginal income tax)

2. Contribute more to Social Security

Increasing your contribution base:

- ✅ Reduces net income → lower income tax

- ✅ Improves your future retirement

- ⚠️ You pay more monthly contribution

Example: Contributing €200/month more = €2,400/year deductible = ≈€720 less income tax (30%)

3. Pension plan

Contributions to pension plans:

- Deductible limit: €1,500/year

- Tax savings: ≈€450 (if 30% marginal income tax)

4. Limited company (SL)

If you bill more than €60,000-€70,000/year, creating a limited company may be worthwhile:

Self-employed:

- Income: €70,000

- Income tax (≈37-40%): ≈€26,000

Limited company:

- Profit: €70,000

- Corporate tax (25%): €17,500

- You pay yourself salary (tax-optimized)

- Potential savings: €4,000-€8,000/year

Important: A limited company has additional costs (accounting, bookkeeping).

5. Apply reduced withholding (first 3 years)

If you've been self-employed less than 3 years:

- Apply 7% withholding instead of 15%

- Better cash flow

- You pay the adjustment in the annual return

6. Invoice at year end vs January

If you invoice on December 31:

- Taxed in that year's return (following April)

If you invoice on January 2:

- Taxed in next year's return (in 16 months)

Advantage: Delays income tax payment without breaking any rules.

7. Correctly deduct working from home

If you work from home, deduct 30% of:

- Electricity, water, gas, internet

- Property tax, homeowners fees

Example: €200/month expenses → €60/month deduction = €720/year → savings ≈€216 income tax

Differences: self-employed vs employee income tax

| Aspect | Self-employed | Employee |

|---|---|---|

| Calculation | On net income | On gross salary |

| Payment | Quarterly (form 130) | Automatic monthly withholding |

| Deductible expenses | Many (computer, training, etc.) | Very limited |

| Tax return | Always mandatory | Sometimes not mandatory |

| Optimization | High (many strategies) | Low (few options) |

👉 Net salary as freelance vs employee

Conclusion

Income tax for self-employed is calculated on net income (revenue - expenses), which allows you to significantly reduce the tax bill.

Keys to paying less income tax:

- Deduct all possible expenses (keep invoices)

- File form 130 on time

- Consider invoicing with withholding

- Optimize fiscally (pension plan, higher contribution)

- Consult a tax advisor (savings of €2,000-€5,000/year)

If you're an employee and want to compare:

👉 Calculate your net salary as an employee

Related guides

Frequently asked questions

Solve the most common questions about this topic

Calculate your net salary now

Get your personalized result in less than 1 minute